The Fed supports the market

May 18, 2020 @ 17:50 +03:00

Last week the American market closed with a decline and failed to fully offset the drop of the beginning of the week. Futures on S&P500 added 0.9% at the beginning of the week. This happens against the background of data on the decrease in retail sales by 16% and industrial production by 11.2% in April alone. All this data is worse than expected.

US companies release very negative reports. Already submitted reports from 90% of S&P 500 companies showed a 64% YoY decline in revenues for the first quarter, which included only a few weeks of the pandemic.

This decline is not in line with market optimism. The growth of stocks is supported by retail investors, as well as the policy of the Federal Reserve. Along with weak economic data, record inflows of money from retail investors are reported. They are in a hurry to buy back the market decline and to bet on the indices due to the improvement of the situation with the pandemic. In an increasing number of countries, restrictions are being lifted, creating a positive news backdrop. But as soon as this driver started to dry up, a new driver appeared in the markets.

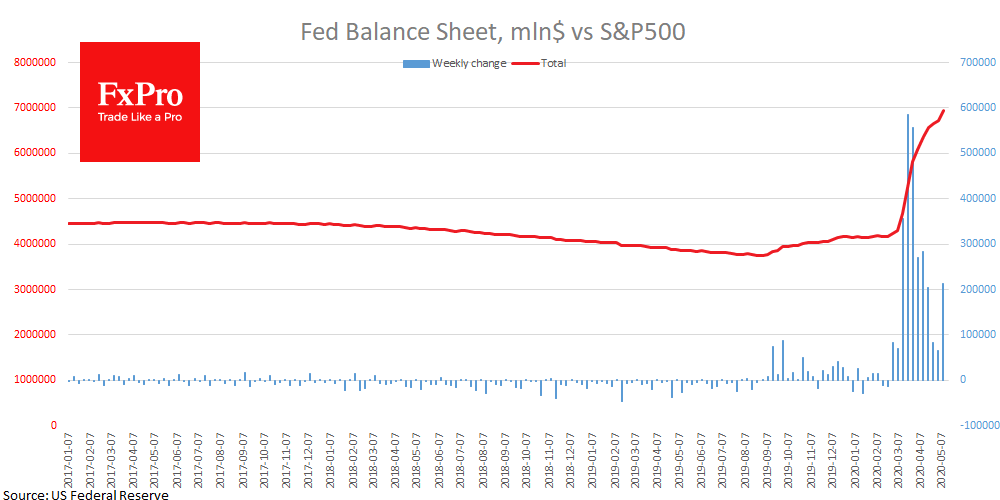

The Fed started a new corporate bond-buying program last week. Weekly data on the Fed’s balance sheet as of Wednesday showed an increase of $212bn ($65.5 billion a week earlier) to nearly $7 trillion. And these purchases seem to be the very force that shifted the market balance in favour of buying.

It happened at the right moment when market optimism began to weaken.

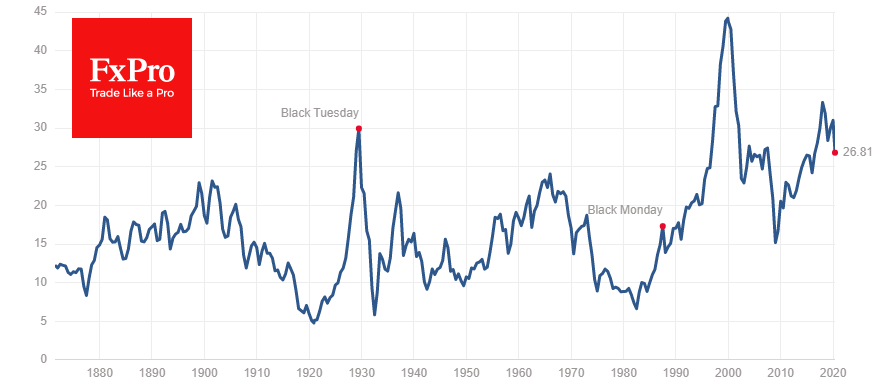

The conservative metric proposed by Nobel laureate Schiller – inflation-adjusted earnings over the past ten years – has just begun its path down. The index rose above 30 just at the peak of the stock market in 1930, during the Dot-com bubble, and the recent rally.

The chart clearly shows that once it reversed to decline from levels markedly above average, this index finds its bottom only after falling notably below average near 16.7. There may be two reasons for the reversal – low stock prices or an increase in earnings from stocks. So far, we do not see any of that. US stock prices are close to September 2019 levels, while corporate profits have just started to decline.

All this speaks in favour of the idea that the stock market remains very expensive for the current macroeconomic conditions, as a sharp decline in earnings per share makes companies relatively more expensive. Even if we take into account that the labour market will not so sharply deteriorate further, it is still a decline that drags people’s incomes down, forcing them to reduce their investments in stocks. The Fed may put out the fire in the markets for a while, but it won’t be able to buy all the bonds on its balance sheet. And it won’t do that. As in 2008, at some point, US politicians will face the question of which companies to rescue and which to let go bankrupt. Twelve years ago it was the bankruptcy of Lehman, but the rescue of AIG.

The FxPro Analyst Team

April 26, 2024 @ 15:17 +03:00

April 25, 2024 @ 17:33 +03:00

April 25, 2024 @ 13:54 +03:00

April 24, 2024 @ 13:03 +03:00