Is there a return in risk demand or the end of the 40-year bull market in treasuries?

October 06, 2020 @ 11:44 +03:00

Trump went back to work in the White House, which supported the recovery of the stock markets. Asian indices reached a 2-week high. Futures on the S&P 500 are again above their February peaks after rising 1.8% on Monday.

Demand for risk assets is spreading outside the equity market, fuelling interest in oil and gold at the expense of bonds.

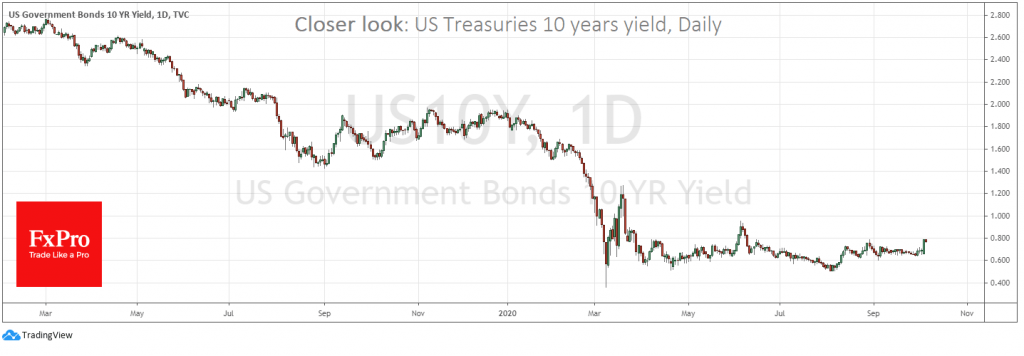

Yields on 10-year treasuries rose above 0.76%, the highest since early June. These yields were consistently above these levels until March when the Federal Reserve starts its extreme rate cuts, and markets flew into the abyss. At that time, trading was a means of saving their capital from the melting stocks and commodities.

For a while, the influx of freshly printed money from the Fed and the public fed stock growth and did not harm bonds. Between April and August, however, ten years of yields seem to have formed the bottom from which they were pushed up last month.

The US bond market is facing an important test in the coming days. The yields of 10-year trader’s bonds may return to the 0.50%-0.75% range. In this case, it will be possible to talk about the renewal of the trends of the previous months: increased demand for stocks of fast-growing (mostly technological) US companies and moderate weakening of the dollar.

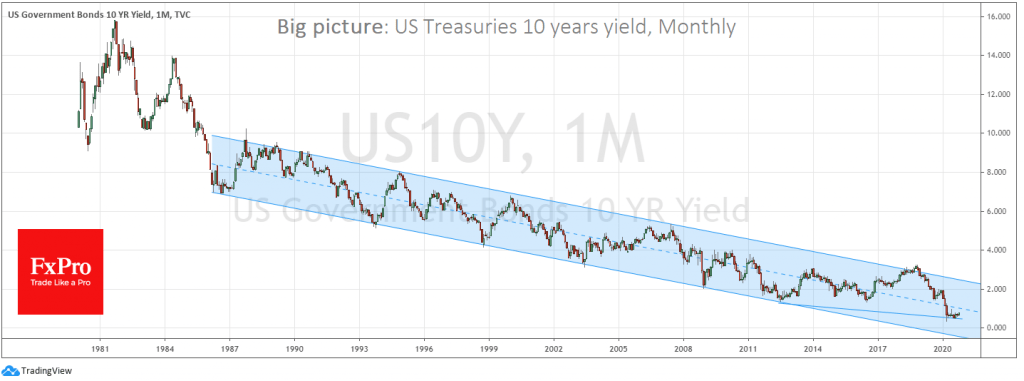

But it cannot be ruled out that we are now seeing the formation of a more dangerous trend. It may well turn out that long-term investors are betting on the end of the 40-year bull market in bonds. Since 1981, the yield on US 10-year bonds has fallen from around 16% to a low of near 0.5% earlier this year.

The decline in bond yields at the beginning of the 1980s triggered a strong pull in the dollar, causing it to grow by 50% against a basket of major currencies. Further, in 1985, representatives of the ministries of finance of these countries coordinated interventions against the dollar. US bonds continued to rise in price, reflecting investor confidence in the strengthening of US economic power.

Classically, an increase in US bond yields can attract the interest of those investors who are trying to find yields higher than those in the US overseas markets. An increase often follows the dollar rate increase.

But what if this is another case? Investors sell long-term US treasuries and look for alternatives abroad, avoiding the fear of being hostage to negative real yields over the next few years or even a decade. In this case, we may see a simultaneous increase in the yield of USTs and weakening of the dollar. This also does not bode well for the US stock market.

Over the last decade, it has grown more substantial than many other markets, being content with increased interest in US financial assets. If investors withdraw capital from the USA, its markets may also be ‘below average’ in term of returns, gradually departing from current objectively inflated levels relative to their foreign counterparts.

The FxPro Analyst Team

April 26, 2024 @ 15:17 +03:00

April 25, 2024 @ 17:33 +03:00

April 25, 2024 @ 13:54 +03:00

April 24, 2024 @ 13:03 +03:00